Global Economic Dynamics and the Role of SWFs

- In Economics

- 04:21 PM, Mar 30, 2016

- Mukul Asher

Overview: The global economic dynamics portends subdued economic growth; elevated public and private debt levels and associated risks; low energy and commodity prices; changing nature of global trade; challenging investment environment; and heightened anxiety and perceived economic insecurity among the population around world. These dynamics have important implications for the role of Sovereign Wealth Funds (SWFs), including the nature and rate of growth in assets, asset allocation between domestic and global sectors, and stakeholder relations, particularly with their domestic population. This lecture discusses these interactions between global dynamics and the role of SWFs, including those SWFs whose asset accumulation is primarily dependent on energy and commodity sectors. This will stress on the rising importance of not having too large and too prolonged divergence between expenditure and revenue commitments of public sector budgets and their links with SWF assets and receipts.

Background:

- The 2008 global crisis and its continuing aftermath, currently being manifested in volatile capital markets, particularly in emerging economies, and the changing nature of global trade with services contributing a greater share to trade growth than manufactured goods, has led to a rethinking of conventional economic policies, and of the role of various institutions, including SWFs.

- Traditionally, SWFs have had externally-oriented investment policies, and the stock of SWF assets and incomes arising from them were more than sufficient to address any fiscal gaps which may arise. This is changing as a result of the current global dynamics, necessitating a major re-think and re-orientation of the role of the SWFs.

- IMF (2008) classifies SWFs into 5 groups:

- Stabilization Funds (designed to insulate the budget and the economy against commodity price swings)

- Savings Funds for Future Generations (to enable conversion of non-renewable assets into a more diversified portfolio of assets and mitigate the effects of Dutch disease)

- Reserve Investment Corporations (these assets are still counted as reserve assets and are established to increase the return on reserves, though at a higher risk)

- Development Funds (designed to help fund socio-economic projects and infrastructure. These funds usually have large domestic component)

- Contingent Pension Reserve (particularly to finance social security and health expenditures for rapidly ageing populations). We will primarily discuss Stabilization funds.

There are no robust databases which monitor the financial flows of the SWFs. Therefore, the estimates of the size of the SWFs vary widely. Total SWF assets as of Dec 2015 were estimated to be USD 7.2 trillion, slightly lower than USD 7.3 trillion in Mar 2015. This represents a reversal in the continuously rising trend of SWF assets observed earlier (USD 3.4 trillion in Sep 2007). 56% of total SWF assets in Dec 2015 were by resource-rich economies, including Gulf countries which accounted for 39% of the total.

Source: IMF WORLD ECONOMIC OUTLOOK (WEO) UPDATE (2016)

Global Dynamics: Elevated Debt

Indicators of the Financialisation of the Financial Sector

- The growth of the financial sector as a percentage of GDP

- The growth of profits of financial institutions as a percentage of profits of all the corporates engaged in economic activity

- The remuneration of managers in the financial sector relative to others, and

- The share of shadow banking systems as well as derivatives in the total activity of the financial sector would be useful indicators of the extent of financialisation of the financial sector

List of vulnerable economies

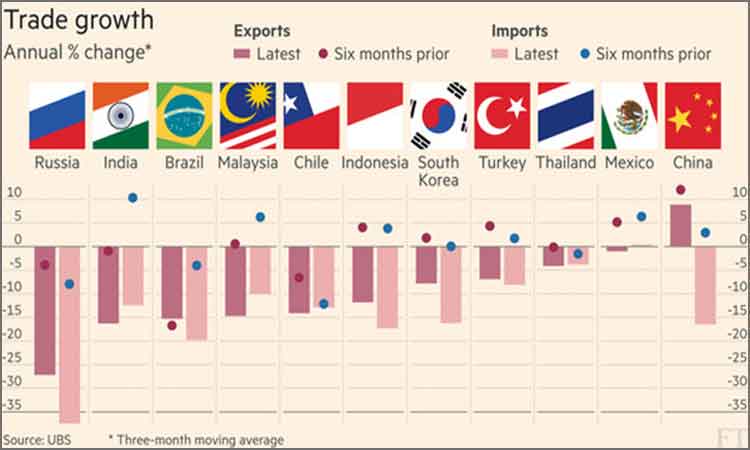

Changing Nature of Global Trade

- There appears to be a shift in the relationship between growth of global trade and the growth of global GDP.

- Global trade has grown nearly twice as rapidly as GDP until 2011.

- However, IMF (2016) projects that in 2014, the growth in world trade volume of goods and services, at 3.4% , was the same as global output growth.

- In 2015, the trade growth recorded 2.6% and was lower than output growth of 3.1%.

- The IMF does not project any marked improvement in this trend over the next 2 years.

- Along with this, the contribution of services in the growth in global trade has been exceeding the growth in goods trade in recent years.

- UNCTAD Estimates that in 2014, service exports accounted for more than 60 percent of the rise in the value of global exports, much higher than the corresponding proportion of 15 percent in the five years to 2011.

- This has important implications for export-oriented economies, particularly those that rely on longer logistics and supply chains and benefit from production networks.

- Disruptive technologies, particularly centring around IT and related developments such as additive manufacturing (AM) may suggest a need for these economies to re-orient their growth strategies.

- The current investment environment is accentuating the challenges for providing retirement income protection for rapidly ageing population around the world.

- The low real interest rate environment is contributing to the tendency to seek excessive risk on the part of the savers and by the asset fund managers, increasing systemic risk for countries and for the global economy.

- As SWFs control major pools of investment funds, this challenging investment environment also impacts them, requiring management response.

Increased Anxieties of the Population

- The 2008 crisis and its aftermath, including unconventional monetary policies resulting in extensive quantitative easing, and very large increases in Central Bank balance sheets, along with subdued growth and changing labour market dynamics in which the share of contract workers in the total labour force is becoming significant, have contributed to rising anxieties in the population.

- In some regions, such as Europe, migrants and refugees are further accentuating anxieties of the resident population.

- Among the manifestations are relatively stagnant real wages for a significant proportion of the labour force and rising inequalities of income and wealth.

- Such anxieties are becoming global, requiring credible response from policymakers.

- Unfortunately, good quality data on these are only available for the United States, and a few OECD countries.

Implications for SWFs

-

The growth in SWF assets and in receipts:

- In the earlier periods, the growth in SWF assets and their rising importance was led by rising commodity prices and growing export surpluses, recycled as a part of SWF assets.

- However, the current global dynamics suggest that the growth in assets is likely to be very modest at best, if not stagnating.

- The reported withdrawals of SWF assets from global asset markets such as Saudi Arabia’s represents an example of this (http://www.ft.com/cms/s/0/8f2eb94c-62ac-11e5-a28b-50226830d644.html#axzz3yQnvrGyS)

- The low interest rate environment has also made obtaining higher real returns without undue risk more challenging.

-

Greater domestic orientation:

- Current global dynamics as noted has heightened anxieties of the population. The SWFs were designed to meet the needs of the future generations, and to prepare for less abundant resources and slower accumulation of export surpluses.

- Current anxieties, however, are necessitating greater urgency to meet the needs of the present generation as compared to the needs of future generations. This is evident in countries with relatively small populations but large SWF assets such as Norway (www.bloomberg.com/news/articles/2015-10-06/norway-budget-proposes-boosting-oil-spending-by-14-nrk-says).

- In some countries, the asset liabilities and currency mismatch of the financial institutions, such as commercial banks and pension funds, may also require support from the country’s SWF; and to such measures as capital controls, as exemplified by China, a country with highest foreign exchange reserves in the world of USD 3.3 trillion (as of Dec 2015).

- In some cases, such as for oil-led countries, as Azerbaijan, recourse to IMF and the World Bank loans is expected. (http://www.ft.com/cms/s/0/9759f42a-c51b-11e5-b3b1-7b2481276e45.html)

-

Increasing importance of greater competency in Public Financial Management (PFM):

- An important element of PFM is to structure medium-term government liabilities with realistic expectations of medium-term receipts.

- This element has become even more crucial with current global dynamics. This is exemplified by Saudi Arabia.

- There is also a need to improve the productivity of capital spending, requiring a host of PFM reforms such as in project management, procurement, and budgeting.

- This also applies to government expenditure in general where the output and outcomes obtained from a given input of financial expenditure merits greater focus.

Conclusions:

- SWFs do provide a cushion and time for dealing with the implications of current global dynamics.

- However, without addressing the challenges discussed, SWFs, by themselves, will be insufficient for meeting macroeconomic and financial stability challenges facing countries

- This is especially the case for those countries that plan to transit from resource-rich and/or investment-export led growth strategy to more domestic demand based strategy.

Comments